Published Feb 25, 2023 | 1:00 PM ⚊ Updated Feb 25, 2023 | 1:00 PM

Tamil Nadu has the best ATM density per one lakh population among the big states in the country, according to the latest RBI data released for the October to December quarter of 2022. In the state, there are 39 ATMs available per one lakh people.

In fact, all southern states have an ATM density per one lakh population which is higher than the national figure of 19.

Kerala has 32 ATMs per one lakh persons, while Telangana, Karnataka and Andhra Pradesh have 31, 29 ands 23 ATMs, respectively.

Many big northern states find themselves at the other end of this spectrum. Bihar has the worst ATM density with just eight machines per one lakh population. Another major northern state, Uttar Pradesh, has just 11 ATMs for every one lakh persons.

Similarly, Jharkhand, Madhya Pradesh, Rajasthan, and West Bengal all have figures higher than the national number.

Even Gujarat finds itself only slightly higher than the national figure with 20 ATMs available for every one lakh persons.

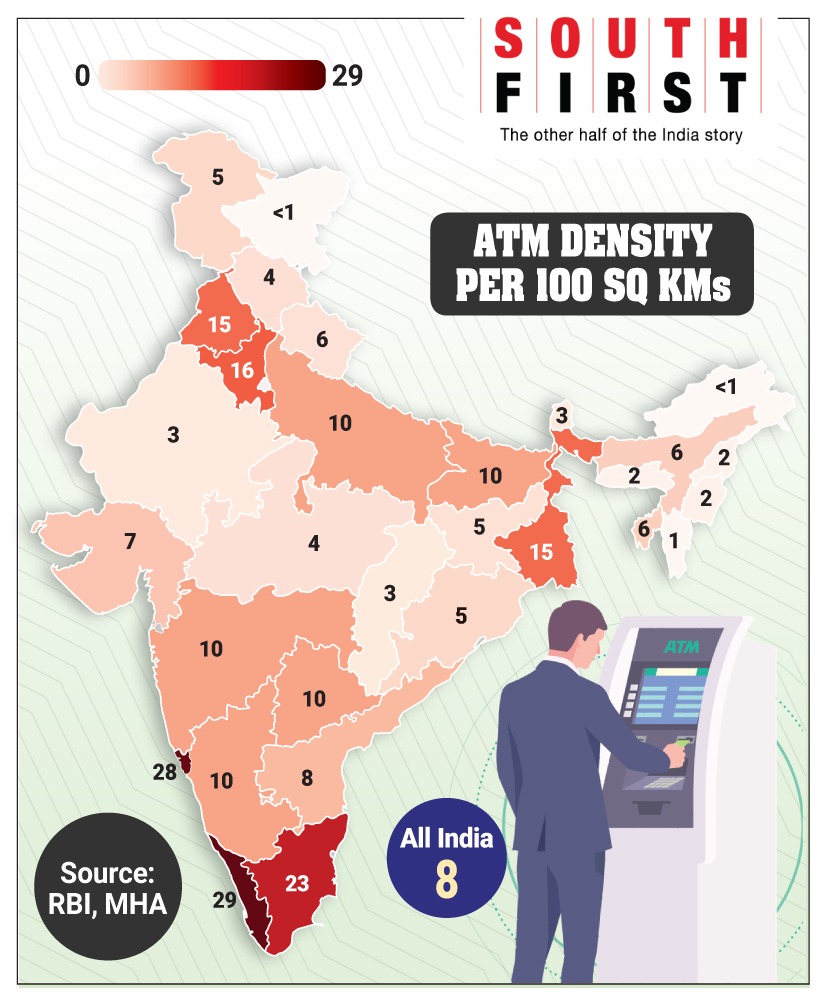

When it comes to ATM density per 100 sq km, Kerala tops the list for big states in the country. In God’s Own Country, one can find roughly 29 ATMs for every 100 sq km.

Except for Andhra Pradesh, whose figure is slightly below the national figure of eight ATMs per 100 sq km, all other southern states find themselves above the national number. Tamil Nadu has 23, while Telangana and Karnataka both have 10 ATMs for every 100 sq km.

Among the big northern states, Uttar Pradesh, Bihar, Maharashtra, West Bengal, Haryana, and Punjab have numbers higher than the national figure. While Haryana leads with 16 ATMs per 100 sq km, Punjab, West Bengal, have 15 each, Bihar, Uttar Pradesh and Maharashtra have 10 ATMs for the same area.

While Rajasthan and Chhattisgarh have the worst density with only three ATMs per 100 sq km, Madhya Pradesh, Odisha and Gujarat all find themselves below the national figure with four, five and seven ATMs per 100 sq km.

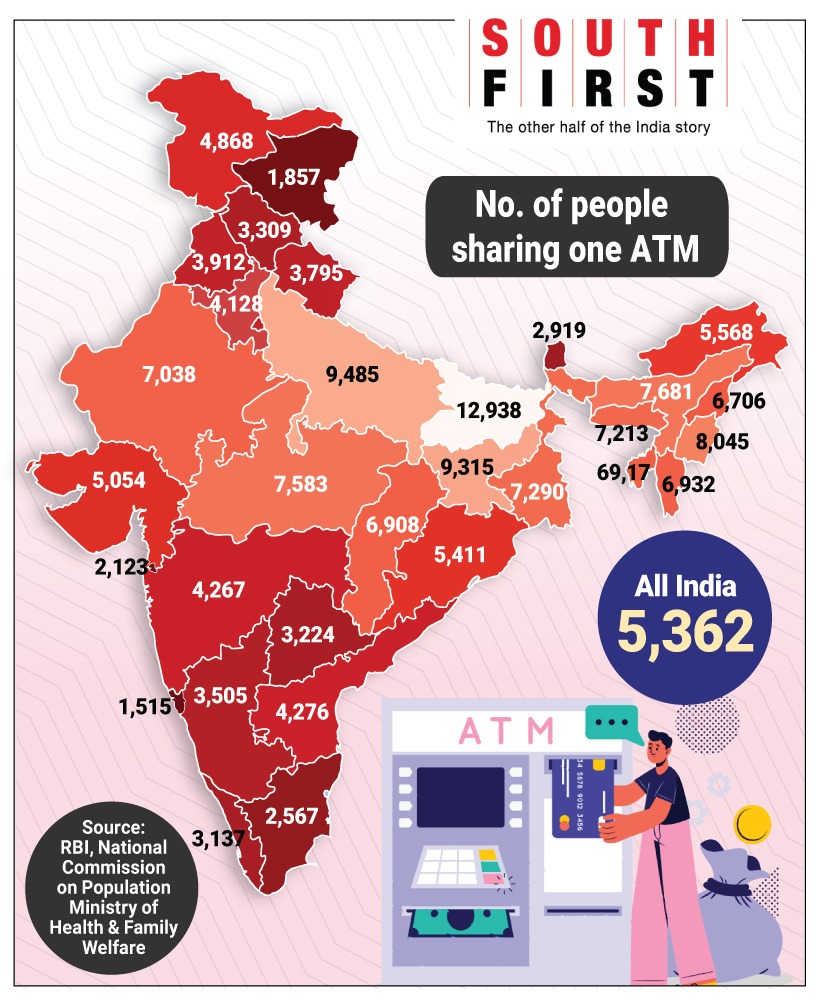

For per capita calculation, population projections for the year 2022 from the “Report of The Technical Group on Population Projection for India and States 2011-2036” published by the National Commission on Population Ministry of Health & Family Welfare has been used.

For per capita calculation, population projections for the year 2022 from the “Report of The Technical Group on Population Projection for India and States 2011-2036” published by the National Commission on Population Ministry of Health & Family Welfare has been used.

It means that people will find themselves in shorter queues outside an ATM. It would also mean people have to travel shorter distances to reach an ATM, at the very least in urban pockets.

Moreover, a high ATM density could be a positive sign, as it would suggest that people in these states have greater access to cash and other banking services, which can help them to better manage their finances and participate more fully in the economy.

However, it’s important to note that a high per capita access to ATMs alone is not sufficient to guarantee of financial inclusion or access to banking services for all segments of the population.

There could still be significant disparities in access to financial services, particularly for those living in rural areas and those from marginalised communities.

Therefore, to correct this skewed access to basic financial services, efforts are needed to improve the overall infrastructure, expand financial literacy programmes, and promote innovative banking solutions that can reach underserved populations.

More importantly, it could be a particular problem for people living in rural areas, where access to traditional banking services is often limited.

It could also be a challenge for low-income individuals, who may not have access to the transportation or other resources needed to travel to an ATMs that is located far away.

It could also be a challenge for low-income individuals, who may not have access to the transportation or other resources needed to travel to an ATMs that is located far away.

To address the issue of low per capita access to ATMs, efforts are needed to expand the banking infrastructure and improve access to financial services in these states.

This could include the deployment of more ATMs in underserved areas, as well as the development of innovative banking solutions, such as mobile banking and digital payments, that can reach people who may not have access to traditional banking services.

India is a rapidly growing economy with a large and expanding middle class, which has led to an increased demand for financial services such as cash withdrawal, deposits, and other banking services including many Direct Benefit Transfers (DBTs) from both the central and state governments.

Additionally, a large part of the Indian population still relies heavily on cash transactions, which further fuels the demand for ATMs.

Although in recent years, the Centre has promoted financial inclusion and encouraged the use of digital payments, cash remains the dominant form of payment in many parts of the country, especially rural areas.