Published Jun 24, 2026 | 11:00 AM ⚊ Updated Jun 24, 2026 | 11:14 AM

Global Capability Centres in India. (AI-generated image)

Synopsis: Bengaluru, Chennai, Hyderabad and all major Indian cities host them. But the reality is India’s Global Capability Centres boom is falling short on productivity, innovation, and high-value work.

A recent NASSCOM-ZINNOV report about India’s Global Capability Centre (GCC) landscape states that India is on its way to being an AI-powered strategic hub–one that earns us USD 98.4 billion in revenue and employs 2.36 million people. It also states that GCC revenue has grown at a Compound Annual Growth Rate (CAGR) of 9.9% since FY21 and its employee base by 6.2%.

The report, however, does not mention that the average revenue per employee is just USD 41,695 and that it has grown at a CAGR of just 2.6% during the last five years. We hear or read headlines like “from cost centre to strategic hub;” “GCC boom explained: 100 billion dollars tech story”; “India the GCC Capital of the World”; “India’s GCC story: Innovating with AI-powered automation, and so on. These headlines are more rhetorical and do not necessarily represent our reality.

One of the key arguments being made is that the GCCs do higher-end work and they are the hubs of technological innovation. A PwC report sees “GCCs assuming a more strategic role while supporting the broader transformation strategies of global enterprises.”

One of the simplest measures for assessing whether the GCCs are indeed playing a strategic role and/or are driving AI-led transformation is the revenue per employee that GCCs are generating – revenue per employee at a GCC is a fully loaded cost per employee, which includes wages and the cost of infrastructure.

If these employees are indeed doing very high-value-adding work, their compensation and fully-loaded cost would be much higher than the IT firms who are doing relatively low value-adding work. We also know that MNCs tend to pay higher than local IT firms and have a higher cost of infrastructure.

The NASSCOM-ZINNOV report estimates that revenue per GCC employee for FY26 was USD 41,695. On the other hand, HCL Tech and Infosys’ revenue per employee is more than USD 60,000. TCS, with the lowest productivity among them, too has an average revenue per employee more than USD 50,000 per annum.

It won’t be wrong, therefore, to suggest that GCCs are not yet playing a strategic role in transformation strategies of global enterprises. Employees who are driving AI-led transformation projects are likely to cost much more even in India, particularly for GCCs. However, the employment numbers, as reported by the NASSCOM-ZINNOV study, have definitely grown faster for GCCs than the Indian IT firms during the last five years.

Another aspect that merits assessment is the size of these GCCs and the industry that these firms come from.

It is very unlikely that 20,000+ employees in India of a large global firm are doing cutting-edge technology work. A finance firm that employs 50,000+ people is unlikely to be doing transformation projects as the above-mentioned reports suggest.

So, be prepared for the reality. In the coming few years, if AI implementation does indeed deliver the expected results, the number of employees required by these GCCs will decline significantly, as these large enterprises will be one of the early adopters of AI technologies.

GCCs remain a cost-arbitrage strategy for these MNCs as the annual cost for similarly skilled employees is possibly three to four times in the US. The cost gap is lower for senior-level employees. And infrastructure costs are not too different between India and the US.

To tweak the famous campaign slogan of Bill Clinton and apply it in this context, “It’s the cost benefits, stupid,” that are driving the GCC investments in India. Not innovation at the moment.

India does have the opportunity to participate in greater value-adding activities of large global enterprises.

We must, however, be able to take core product leadership, customer-facing innovation, and regulation-intensive work, which requires us to go beyond engineering, back-end platform development and operations and support work. If we cannot make this transition, relabeling captives to GCCs will neither accelerate growth nor build capabilities that will allow India to become a high value-adding player in the global technology value-chain.

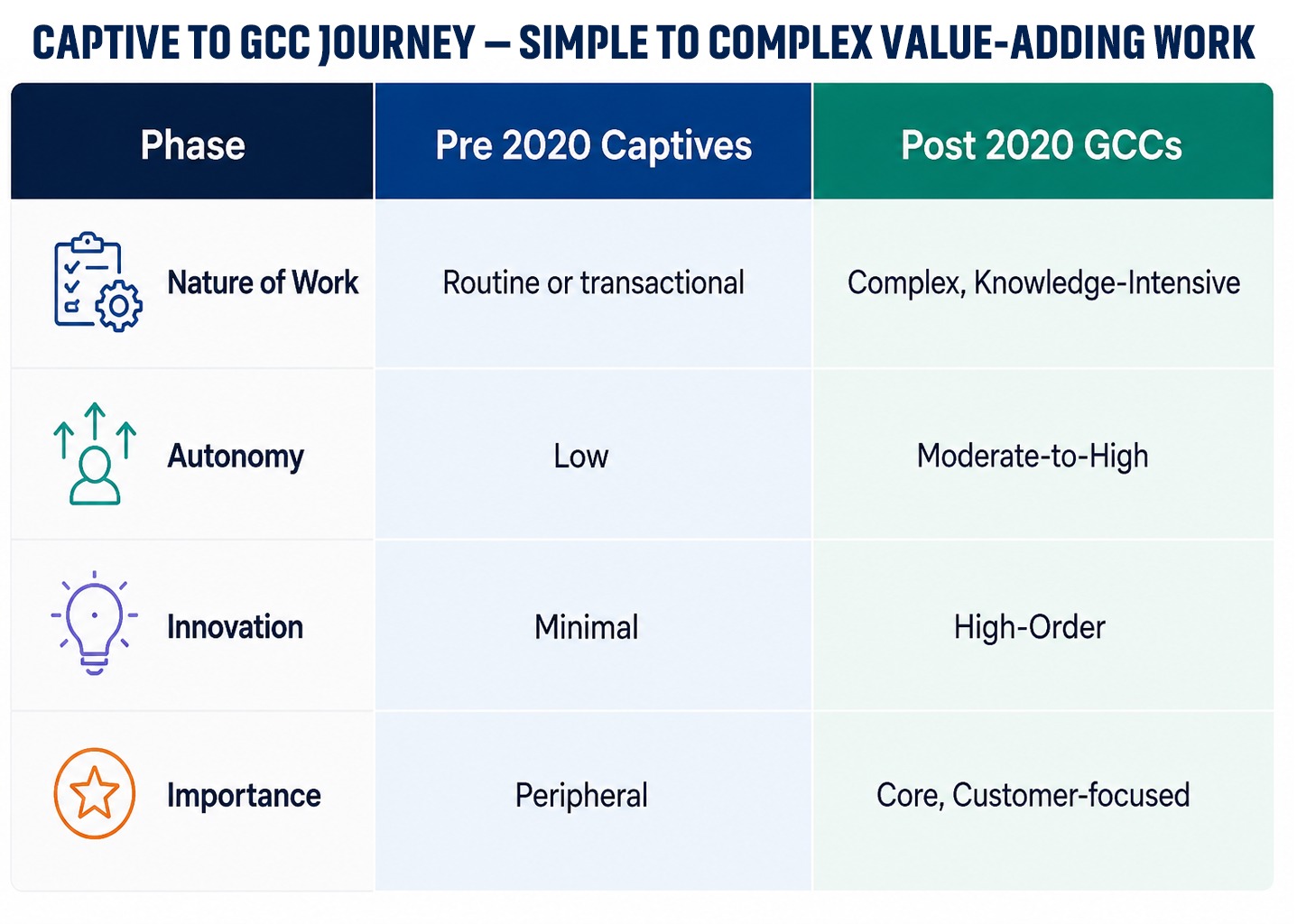

The table below outlines the changes that Indian leadership teams at GCCs, our universities and colleges, and our students and experienced managerial and technical professionals must make.

India’s transformation to a global GCC hub will require a higher share of employees being architects, data scientists, and product managers. Leadership roles in India will need to be redefined to include creation of product roadmap, capital allocation, and customer interface.

India’s transformation to a global GCC hub will require a higher share of employees being architects, data scientists, and product managers. Leadership roles in India will need to be redefined to include creation of product roadmap, capital allocation, and customer interface.

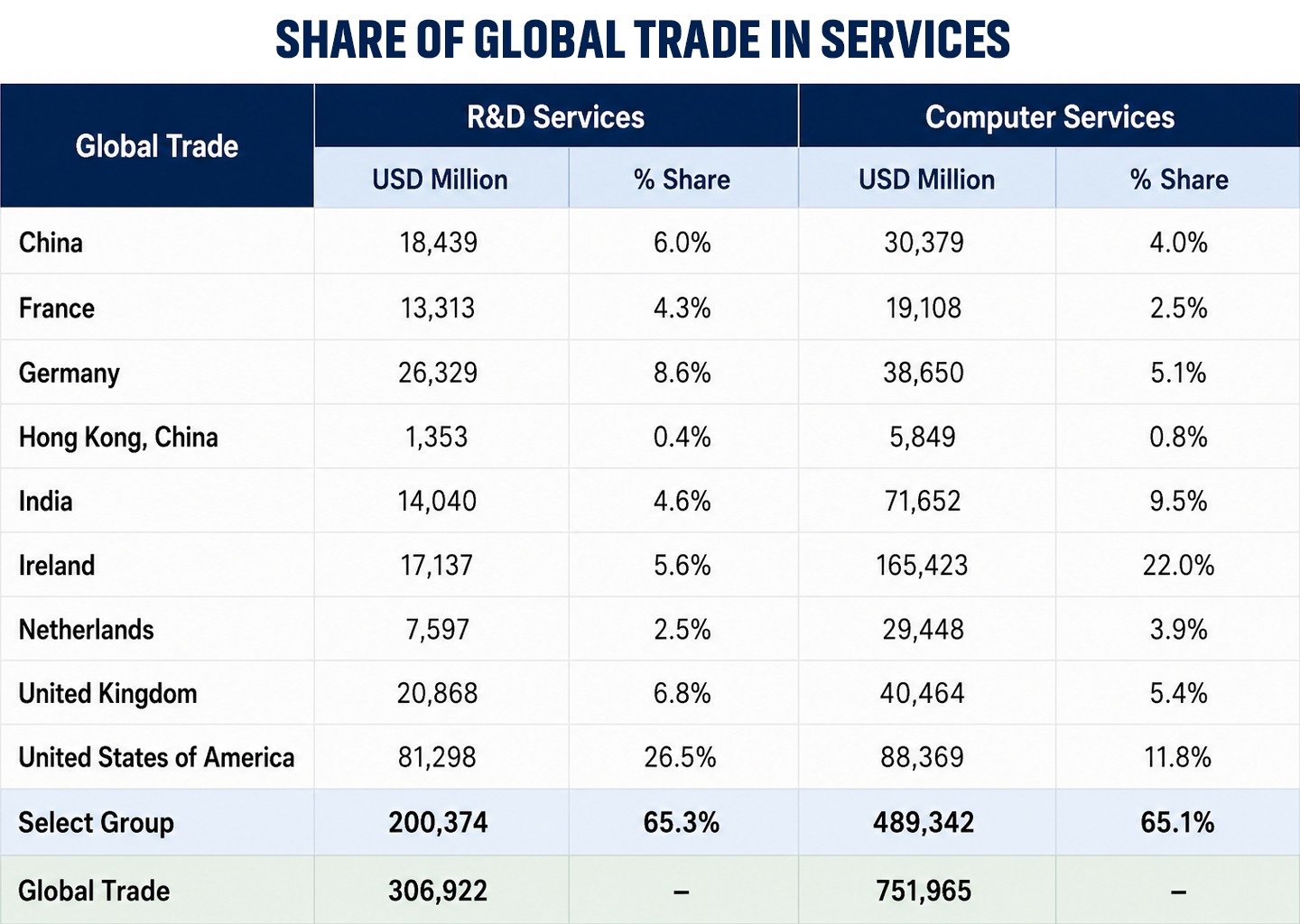

A majority of the Indian GCCs still need to make a transition from low-value execution to mid- or high-value integration with global production and innovation networks. An analysis in Table 2 of global trade in services demonstrates that we are yet to play a vital role in the R&D Services value chain, though we are reasonably well placed in the computer services value chain.

In short, GCC work has become more skilled, but remains largely structured rather than deeply complex or ambiguous. We must, therefore, move away from managerial rhetoric and language inflation to building capabilities for solving ambiguous problems where tacit knowledge and judgment-based decisions are more important than doing codified work.

Also Read: When banks like HDFC fail customers, don’t dismiss it as a mere glitch

(Edited by R Rajesh Kumar.)