Published Jun 11, 2026 | 8:00 AM ⚊ Updated Jun 16, 2026 | 7:40 PM

Can Zepto turn profitable? Is Rs 8010 rore too big a price to pay?

Synopsis: Quick commerce is a low-gross-margin business, by its very nature. It is a quick cash guzzler too. Are expectations of growth then exaggerated?

Zepto’s Rs 8010-crore IPO has once again led to strong arguments about the potential for growth in the Indian organised retail and e-commerce market. It comes at a time when large established firms are struggling to grow, and platform-based consumer-serving businesses are sliding down from hyper-growth to the struggling-for-growth stage.

While many of these businesses grow much faster than the rest of the segments in the broader industry, they experience slow growth even before they have achieved break-even sales. They burn private as well as public equity capital—equity that is scarce. This is close to being a sin in a low-middle-income country. We have far better uses for risk capital in the country.

The true size of our e-com consumers

India is a low middle-income country, with nearly two-thirds of our population living in rural areas, which implies that the number of urban households ranges between 120-130 million. In its recent quick commerce industry report, Redseer estimates the consuming class to be about 230 million households.

Given that e-commerce and quick commerce are largely fulfilling an urban need, the target market for quick commerce is much smaller. These businesses serve consumers who live in high-traffic-density areas and will struggle to shop for their daily needs and, therefore, are willing to pay for convenience.

One of the determinants of demand for quick-commerce services is the monthly per capita consumption expenditure.

Median monthly per capita urban consumption is Rs. 5,622, with the average being Rs. 6,996. It is very unlikely that an urban consumer with monthly consumption expenditure of Rs. 5,622 would be a regular customer for a quick commerce business, which rules out 50% of 120-130 million customers.

So, it’s difficult to see the target consumer base for quick commerce as being anything more than 60 million households. The Redseer report too estimates that the number of annual transacting customers ranges between 75-85 million.

Is India truly a growth market for quick commerce?

Redseer estimates the quick commerce market to be Rs. 1 trillion, implying an average annual purchase of Rs. 13,000 per household for 75 million households.

Even if we assume that there is more than one transacting customer per household, the industry is probably already close to reaching its potential customer base. Some of these customers are possibly using e-commerce platforms like Amazon and Flipkart for their quick delivery needs and, therefore, are likely to need greater incentives to switch to independent quick-commerce players like Zepto, Blinkit or Swiggy.

Once the initial high-growth period ends, independent players like Zepto will need to focus on gaining a higher share of retail wallet through expansion of their product portfolio, with increasing share of sales coming from higher-value goods. Once they start offering a greater range of higher-value products, the relevance of the quick delivery value proposition will decline.

Quick-delivery value proposition is largely relevant for perishable and semi-perishable goods and a few impulse products. Consequently, the current hyper-growth phase will turn into a normal growth phase, as has been the case with the food delivery business, where gross order value and number of transacting customers are growing between 15-20% and average order value is nearly stagnant.

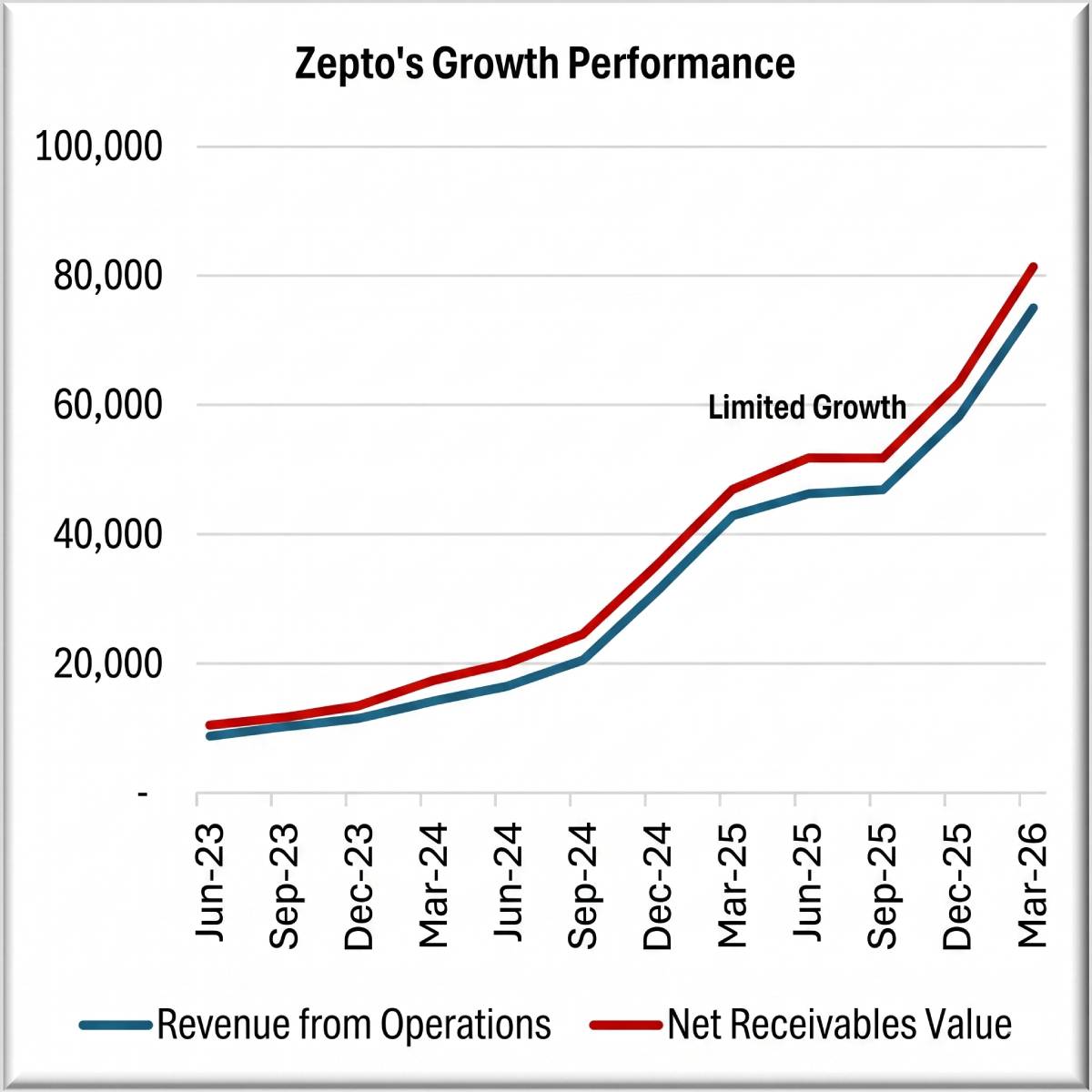

Zepto’s growth and cash burn performance

In Zepto’s case, the signs of the slow growth phase have already appeared during the first three quarters of 2025, where its total income as well as net receivable value had stopped growing.

Zepto has, however, been able to accelerate growth and slow cash burn during the last two quarters, which coincided with its filing the draft prospectus for raising fresh equity.

Growth has been driven by growth in order volume and revenue through brand advertisements on its platform. The increase in store counts has also contributed.

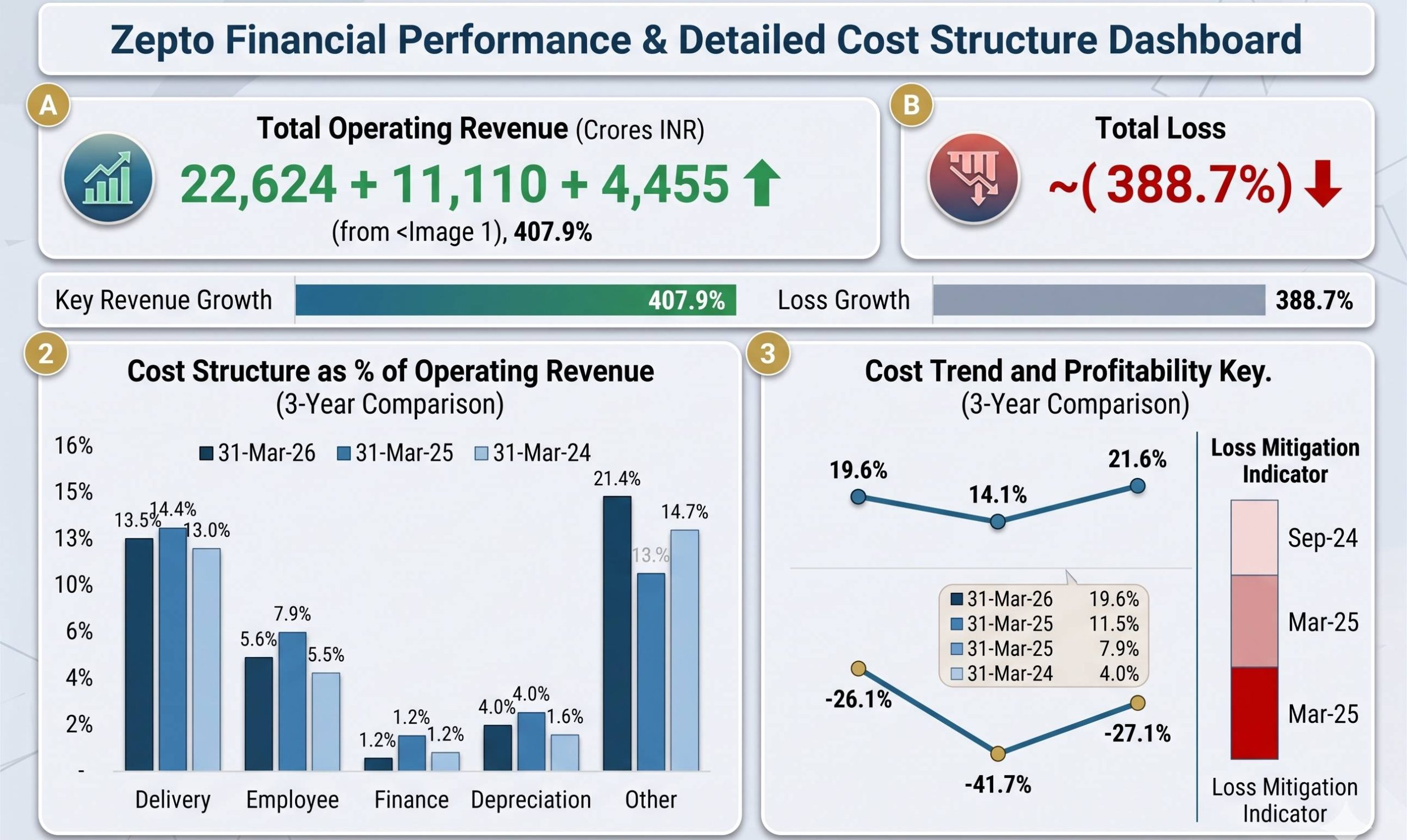

It has conserved cash through better working capital management. However, its total cash burn through operating losses continues to be Rs. 1,000 crore per quarter. It also expects to continue burning cash, as it plans to use Rs. 1,734.9 crores of equity capital for meeting rental costs of existing dark stores and another Rs. 1,629 crores for opening new stores.

In short, quick commerce is a quick cash guzzler too.

How is Zepto managing its profitability?

Zepto’s operations too are cash-guzzling, as it has incurred a loss of Rs. 11,744 crores during the last three years.

A decline of this magnitude can happen only if the business is discounting prices or selling low-margin products. Zepto does not seem to have any leverage in the delivery and handling costs too, even though its sales have grown 4x during the last three years.

The only cost element that has come down is employee costs, but that too during the last few years. Since speed increases costs and risk (operations as well as delivery partner health and wellbeing), an excessive focus on speed can hurt the brand and cause loss of trust among customers and delivery partners. Once more, it continues to guzzle cash in operations with no or very limited operating leverage.

What can help the quick commerce market grow?

Given that quick commerce is serving high-frequency, low-consideration, impulse consumption, its economics is driven by the efficiency of its operations and its cost of goods. It is a low-gross-margin business, by its very nature.

The only way it can raise its margins is if it can generate demand for high-value impulse and discovery-led products. It will remain a cash-guzzling business if it ends up being a top-up grocery channel or fulfils demand for low-value real-time consumption. Once it moves to selling higher-value goods, its core proposition of quick delivery may become irrelevant.

Given that Zepto and other firms are already claiming to serve 40-50 million customers, expansion of market coverage to gain new customers is unlikely to drive growth or profitability. Increased store density can improve service, but Zepto and other players in the market must be able to recover additional costs from their customers.

If these businesses intend to monetise their customer base through advertising, as Amazon has been able to do, they need a customer base with high value-adding consumption. If not, the advertising revenue too will stagnate after the initial hyper-growth.

In summary, the quick commerce business in India is possibly heading towards a phase where the hyper-growth period is coming to an end. The existing players will have to focus on improving the economics of their business rather than on growth by burning cash.